Office rents have been severely affected by COVID since early 2020, particularly in Sydney and Melbourne.

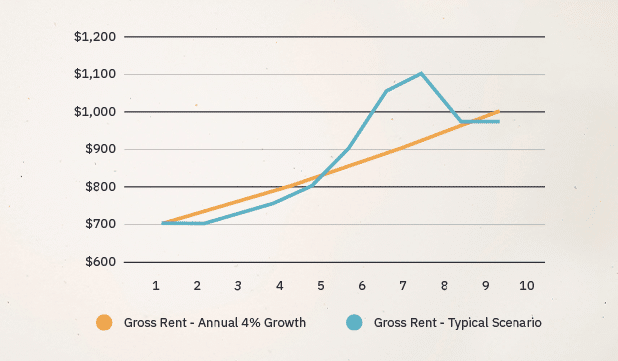

We have considered below a comparison between a ‘benchmark’ B Grade office rent in Sydney CBD, grown at 4% per annum between 2012 and 2021. We have compared this to typical market growth for the same tenancy on a gross face basis.

Sydney – Gross Face Rents

Click graph to enlarge.

This demonstrates a significant uplift in face rents between 2017 and 2019 (years 6 to 8) as demand increased at the same time that a significant amount of office space was withdrawn from market.

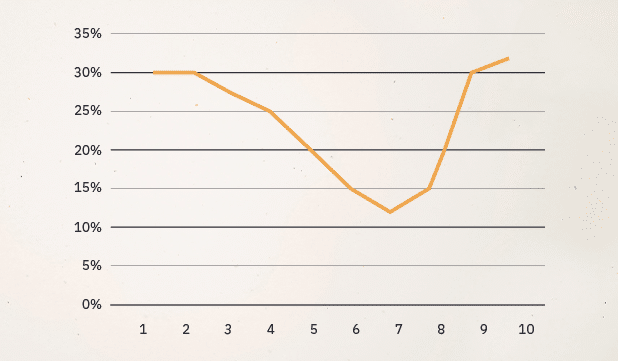

Typical office incentives are plotted as follows:

Gross Incentives

Click graph to enlarge.

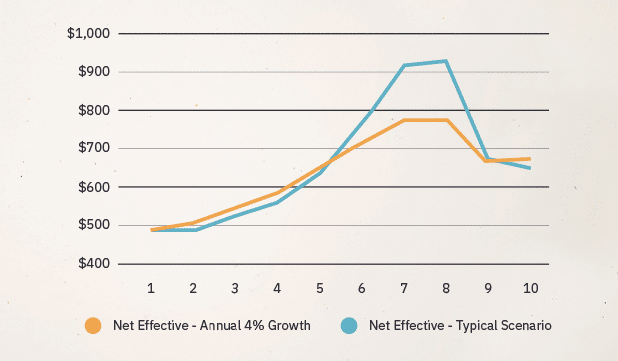

The graph below compares the same rental income streams as the first graph, but on a net effective basis.

Sydney – Net Effective Rents

Click graph to enlarge.

This clearly shows the spike in net effective rents between 2016 and 2018 as the market swung dramatically in favour of landlords.

This also illustrates the decrease in typical B Grade face and effective rents over 2020 and into 2021.

Interestingly, based on our research, rents appear to have fallen to a point that is reasonably in line with the benchmark ‘4% per annum growth’ case.